Bending the Third Rail

Because We Should, We Can, We Do

Cost of the War in Iraq

(JavaScript Error)

Sunday, February 04, 2007

Debt

There's a dramatic article written in Market Observations about the state of household liquidity, baby boomers retirement and it's implications for investing. In short, the article points out that American households are going into debt at historic levels:

For emphasis. This chart is a measure of the amount of ready cash people have available when debt is subtracted. OUCH! Other charts show that the "home equity ATM" is also drying up.

Looks like a house of cards to me that could tumble into a heap. Let's make a couple of assumptions. For most baby-boom workers, pension are going out the door. Some have saved, most have not (see the charts). The largest asset continues to be home equity, although that's been depleted significantly. Debt service is at historic highs. Retirement age is approaching. So what happens to these individuals who are used to living high-off-the-hog as their medical costs rise and incomes drop? And what happens to the economy as a big chunk of people sell their homes and 401K stocks for retirement cash/living expenses? And what do they do with the liquidated assets for security?

This all seems to be suggesting, in the longer term, a depression in housing and the stock market (and likely the overall economy) and a huge rally in bonds. Not tomorrow. Not even this year, but with the impact beginning surely within five years.

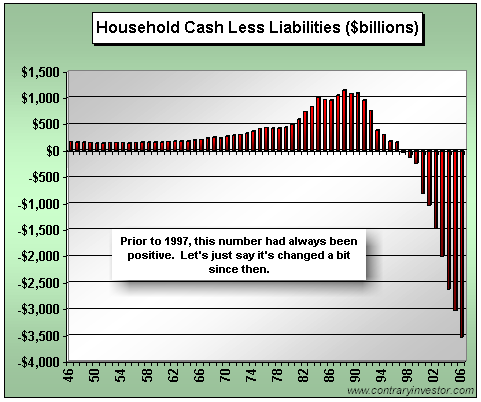

As we've mentioned many a time, what we are seeing in these charts is an intergenerational change in attitudes toward leverage [debt]. It's a change in comfort with leverage. But we will be the first to admit, in nominal dollar terms, the magnitude of the change you see above is more than a bit striking. Much more, as a matter of fact.This chart I found most dramatic:

For emphasis. This chart is a measure of the amount of ready cash people have available when debt is subtracted. OUCH! Other charts show that the "home equity ATM" is also drying up.

Looks like a house of cards to me that could tumble into a heap. Let's make a couple of assumptions. For most baby-boom workers, pension are going out the door. Some have saved, most have not (see the charts). The largest asset continues to be home equity, although that's been depleted significantly. Debt service is at historic highs. Retirement age is approaching. So what happens to these individuals who are used to living high-off-the-hog as their medical costs rise and incomes drop? And what happens to the economy as a big chunk of people sell their homes and 401K stocks for retirement cash/living expenses? And what do they do with the liquidated assets for security?

This all seems to be suggesting, in the longer term, a depression in housing and the stock market (and likely the overall economy) and a huge rally in bonds. Not tomorrow. Not even this year, but with the impact beginning surely within five years.

0 Comments:

About Me

- Name: Greyhair

- Location: Wine Country, California

I'm a very lucky person with every allergy known to man but still happy to be enjoying a wonderful life living in the best place in the world!

Blogroll

The Big PictureBillmon

Blah3.com

Born at the Crest of Empire

Eric Alterman

Eschaton

FireDogLake

Feingold's Blog

Dan Froomkin

The Huffington Post

Hullabaloo

The Illustrated Daily Scribble

Jesus General

Juan Cole

Matilda's Advice and Rants

Mia Culpa

MsJan Quilts

Needlenose

The Oil Drum

Political Animal

Political Wire

Spooks of the Ozarks

Talk About Corruption

TalkLeft

Think Progress

War and Peace

The Washington Note

Other Resources